Don’t Buy The Grayscale Ethereum Trust (ETHE:US)

When the Grayscale Bitcoin Trust (GBTC:US) began trading, many investors made great paper profits from the premium that it carried in the early years. This knowledge enticed the same accredited and institutional investors, as well as others eagerly sitting on the sidelines, to jump into the Grayscale Ethereum Trust (ETHE:US). However, it is not the same because the fundamentals of Bitcoin and Ethereum are not the same. There is no one size fits all investment strategy that encompasses all cryptocurrencies.

Closed-End Funds and Premiums

Many investors do not understand the mechanics and nuances of closed-end mutual funds and trusts. This extends to institutional investors as well. Having launched and managed numerous closed-end mutual funds and trusts, I have learned the granularity of their many pitfalls as well as the opportunities in these instruments.

It is important to examine the premium to the Net Asset Value (NAV) or the price per share compared with the value of the underlying asset. In the case of the ETHE:US, an open-end investment trust, it is Ether (ETH). ETHE:US has recently traded in a range of 6x-10x premium (or 600% — 1,000%) to the NAV. Two weeks ago, on June 11th, grayscale.co reported that the market price per share of ETHE was about $218 and ETH holdings per share were estimated to be $23.03. This means that as a retail investor, you are paying a premium of over 1000% or about $100 for $10 worth of ETH. As a comparison, on Kraken’s cryptocurrency exchange, you can pay $100 for $100 worth of ETH during the same time period. If you were a prudent investor, you would understand that purchasing ETHE:US and disregarding the premium to the underlying spot market is a poor investment decision.

Premiums do not always reflect the future value of an asset. In normal markets, a bond closed-end fund will trade at a premium because the market wants access to the underlying bonds when interest rates go down. It sells at a discount when interest rates go higher. Equity closed-end funds are a little trickier as it is easy to replicate the underlying unless options contracts are involved. However, even with the equity and bond examples, there is a greater premium or discount to future values depending on market volatility.

Premiums often collapse when the market has volatility.

Grayscale funds trade at massive premiums because people just don’t know any better. They buy the trust thinking that it accurately reflects the price of the underlying assets of Bitcoin (BTC), Ether (ETH), and others. We even speculate that recently, retail investors may have been confused with the price of ETH vs ETHE:US, as the price of ETHE:US was as high as $240 on June 11, when ETH was at $220, despite the fact that it was trading at a 1,000% premium to its per share NAV of $23. One thing is certain about these closed-ended instruments: high premiums always collapse, and in this case, investors will be harmed. This has just proven true for any ETHE:US retail buyer on June 11. The ETHE:US premium has collapsed by 60% in the last two weeks to a price of $84.50. This means that you lost 60% of your investment in a two-week period, rather than staying relatively flat if you had owned ETH outright.

Brad Mills explained that “because the price of ETHE rose so high, it started appearing like it was the price of ETH at a discount. Retail investors buying ETHE at $200 aren’t getting a discount at all; rather they are effectively paying $2000 per ETH, when they almost certainly think they are getting a deal on ETH. I think it’s safe to assume the 500–1000% premium is due to a perfect storm: buyers are a combination of FOMO institutional investing, market manipulation by holders of the constrained supply of only 3% liquid ETHE, retail traders getting hosed thinking they are getting a deal on ETH, and maybe a few simple investing for the convenience of not holding keys and tax savings. I think it’s going to end very badly for retail investors and probably a class action lawsuit against Grayscale for allowing this to happen.”

Corporate Structure

The trust structure that Grayscale uses is similar to a closed-end fund but with some annoying nuances. First, closed-end funds are a Regulated Investment Company (RIC), which means that 40% of its underlying assets must be securities. Grayscale Trusts will not work in that structure because none of the underlying crypto assets are securities.

Many people describe trusts working as a casino. I think it is more like a Hotel California. You can put money in to create additional trust shares but you can never redeem them. As Greyscale’s website explains, you can never redeem for the underlying cryptocurrency. You can only sell your shares to the next lucky buyer after your lockup period is over. Closed-end funds do not have these lockups. They also allow you to add structures to enable redemptions.

Finally, trusts are taxed as partnerships, meaning you have to file the Schedule K-1 document, even if you own them in a retirement account. Schedule K-1 forms can lead to more complex and potentially more costly tax preparations each year because some categories of income may be taxed as capital gains, while others are taxed as regular income, and for an investment in an IRA or 401(k), you may also need to pay tax on distributions received. Close-end funds often deliver a more favorable tax treatment to shareholders as well as tax-deferred distributions.

Given the deficiencies in the features of the trust, an investor could be correct about the underlying price action of ETH and yet still lose money.

ETH is a Poor Investment

ETH itself is a poor investment as proposed in our prior paper, Ether And Bitcoin Are Not The Same. The most important part of this paper is explaining the network effect. As the number of users increases and the Ethereum network supporting more dApps grows, then Ethereum becomes more valuable, which improves the network, which decreases gas costs.

Technological advances dictate prices decrease.

It is no different from cell phones. As the network and competition grow, the amount of data transferred increases, while the cost to transfer that data decreases. This is a simple economic theory of supply and demand, examining where the curves intersect. Technology shows greater depreciation of price following demand. Shifts in the supply curve are usually the result of advances in the technology that reduced the input costs of production. This has been true for technologies such as televisions, computers, cell phones, and wired/wireless data. It will also be true for blockchain.

Technological advances that improve production efficiency, such as ETH 2.0, will shift a supply curve to the right. The cost of production decreases and consumers demand more of the product but at lower prices. This has proven true for the price of ETH over the last two and a half years; as the network grew in earnest, prices have dropped significantly despite speculative buying.

An often-heard argument against developers and dApp users demanding lower prices on Ethereum is the fluctuation of gas costs priced in ETH. While the price of ETH is variable, the amount of gas can go up or down as a function of ETH price and network demand. However, this is a failed theory. First, adjustments in gas prices, at best, keep ETH prices stable over the long term, which is an argument against investment and speculation in ETH going higher in USD terms. Secondly, if gas prices can simply adjust to promote users at a lower cost on the network, any true relationship of the price of ETH to the use of the Ethereum network is broken, and the argument that buying ETH is buying the growth of the Ethereum network is void.

Because of this, ETH cannot serve as a means of exchange, unit of account or store of value and therefore cannot be seen as a viable currency. Therefore, ETH is only a speculative asset for speculation’s sake, with no true underlying fundamentals.

ETH Price and Network Growth

As of the date that we are writing this article (June 25, 2020), ETH is trading at $233. If you bought ETH a year ago, you lost 37%. Two years ago, you lost 49% and three years ago, you lost 24%. Of course, many people bought between Oct 2017 and August 2018, losing up to 93%. Retail investors buying ETHE:US a year ago have lost 31%.

During the same time periods, The Ethereum network has grown:

- 3 years ago: 449 dApps

- 2 years ago: 1515 dApps

- 1 year ago: 2854 dApps

- Today: 3479 dApps

It is important to note that Dapp growth began heavily in January 2017, when ETH was $1419.

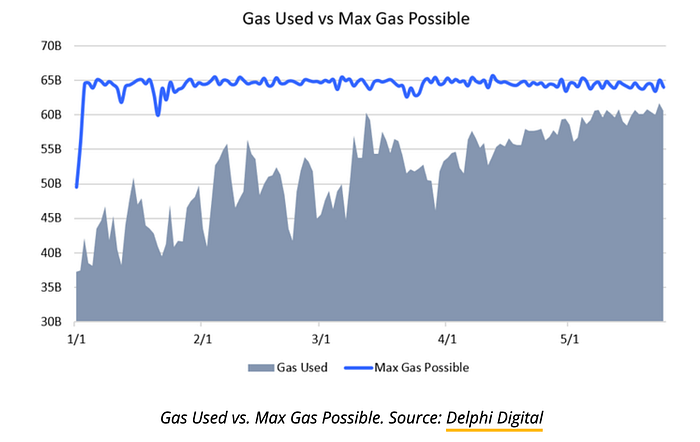

Ethereum daily gas usage has increased since mid-2017 and has accelerated in recent months as on-chain transactions grew and became more competitive. Ethereum network use has hit a new all-time high, which is why the Ethereum community has recently been debating raising the block size limit. The network utilization chart, which depicts the average gas used over the gas limit in percentage, has currently surpassed 95%. Ethereum’s growing adoption is proving to be its Achilles’ heel.

The issues inherent in gas costs have created congestion, which is a negative network externality. Congestion on Ethereum has led to poor user experience, especially for traders in this highly volatile environment, as their leveraged positions may be liquidated before they can act. Ethereum has created a Braess’ paradox, which suggests that adding one or more roads to a road network can slow down overall traffic flow through it. Ethereum currently has a congested highway as well as expensive toll booths which have created an unpleasant experience with drivers looking for alternative routes.

Valkyrie Funds

Steven McClurg — CIO

Leah Wald — CEO

Valkyrie is a discretionary global macro investment management firm. By analyzing fundamental macroeconomic, geopolitical, and social factors we are able to listen to the markets and effectively manage risk and generate alpha.

Valkyrie believes that shifts in government economic policies, political climates, currency exchange rates, international trade, international relations, and interest rates impact all financial markets. Utilizing this expertise of the global economy and financial markets, Valkyrie has constructed unique portfolios with a dynamic macro edge that includes exposure to emerging asset classes.

Together, Steven and Leah utilize macroeconomic strategy to structure and manage portfolios.

About Steven McClurg (CIO):

Steven McClurg is the Chief Investment Officer at Valkyrie. He was a managing director at Galaxy Digital, through the acquisition of his previous company, Theseus Capital, where he was a founding partner and CEO/CIO. Steven started his asset management career at Guggenheim Partners, a leading global investment and advisory financial services firm, where he was managing director and portfolio manager, including oversight of Emerging Markets and Sovereign Credit.

About Leah Wald (Portfolio Manager):

Leah Wald is the CEO at Valkyrie. She was a Partner at Lucid Investment Strategies, an asset management firm specialized in investing in macroeconomic trends. Prior to joining Lucid, Leah was at Vital Financial analyzing investment strategies for Japan, Asia, Middle East energy, and global macro strategy. Leah started her career working at the World Bank Group reporting directly to the former Vice President of the Africa Region.